Historic Stream Family Collection Heads to Christie’s Auction

A remarkable private collection spanning generations of American collectors is set to headline a major auction at[…]

WDC President Says “We Need To Finish The Job” On Conflict Diamonds As Debate Over Kimberley Process Expands

For many producing countries, the concern is not simply ethics but sovereignty. The central issue remains whether international[…]

The Natural Diamond Council has strongly rejected recent claims by Pandora

The Natural Diamond Council has strongly rejected recent claims by Pandora that lab-grown diamonds carry a carbon[…]

Steep Rise in De Beers Rough Production

De Beers says rough diamond production increased by 17% in the first three months of 2026, to[…]

Rough Diamond Jewellery Gains Momentum in the UK and USA

A clear shift is underway across the jewellery markets in the United Kingdom and the United States,[…]

Production Rises, Prices Fall, and Technology Redefines Trust in Diamonds

De Beers reported a 17% year-on-year increase in rough diamond production for Q1 2026, reaching 7.1 million[…]

ALROSA Shifts Strategy as Investment Diamond Sales Surge 40%

Russia’s state-backed diamond giant, ALROSA, has reported a sharp rise in demand for investment-grade diamonds, with sales[…]

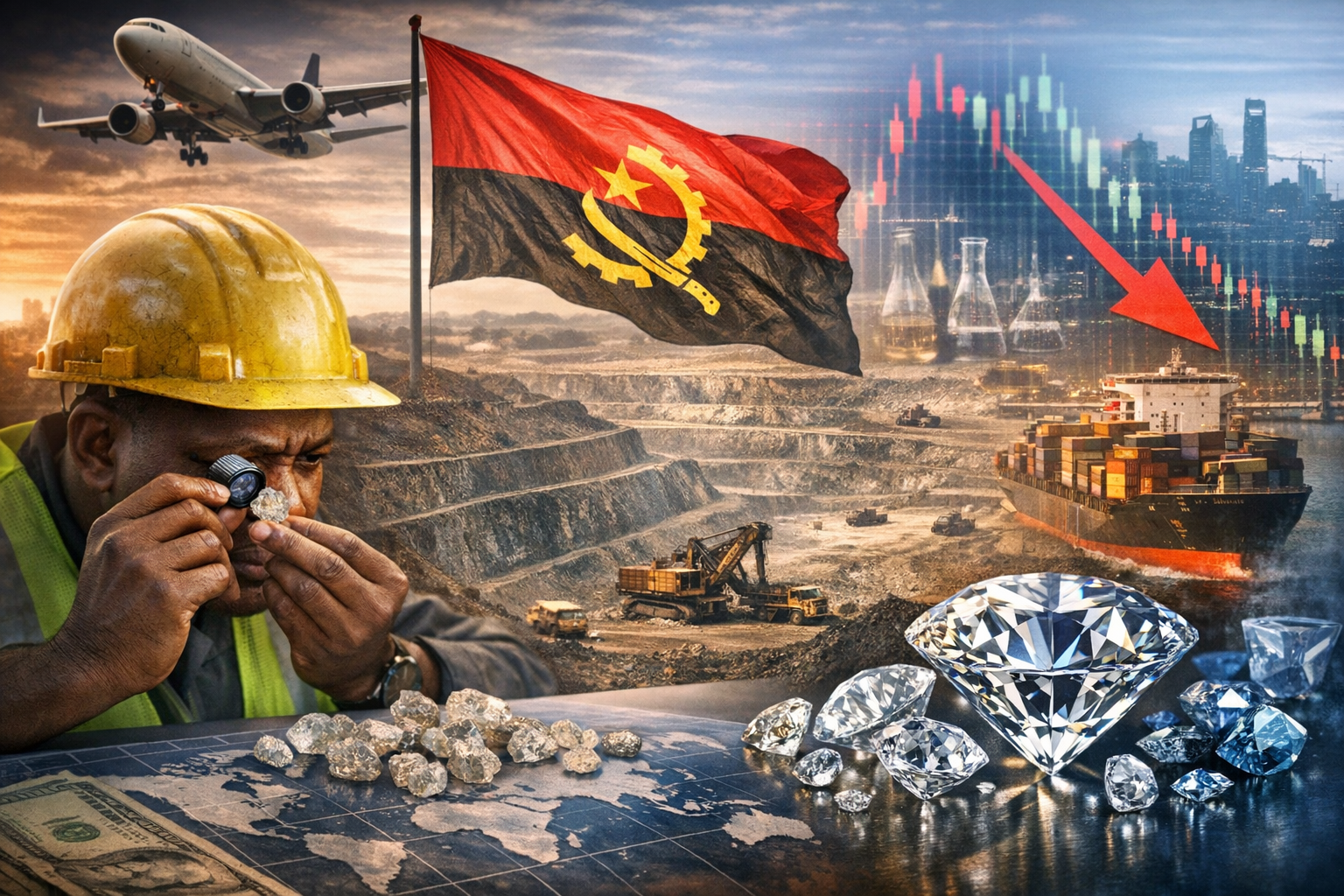

Angola’s Rough Diamond Production Climbs in 2025 as Market Pressures Persist

Angola’s diamond sector delivered a stronger-than-expected performance in 2025, with rough-diamond production rising by 8% year-on-year despite[…]

Hublot Unveils a Diamond Masterpiece: Big Bang Impact One Million

Renowned for its million-dollar horological statements, Hublot once again elevates the intersection of haute horlogerie and high[…]

Diamond Debut for De Beers and Sotheby’s Collaboration

The sale of the Jwaneng 28.88 diamond later this month marks the start of a collaboration between[…]