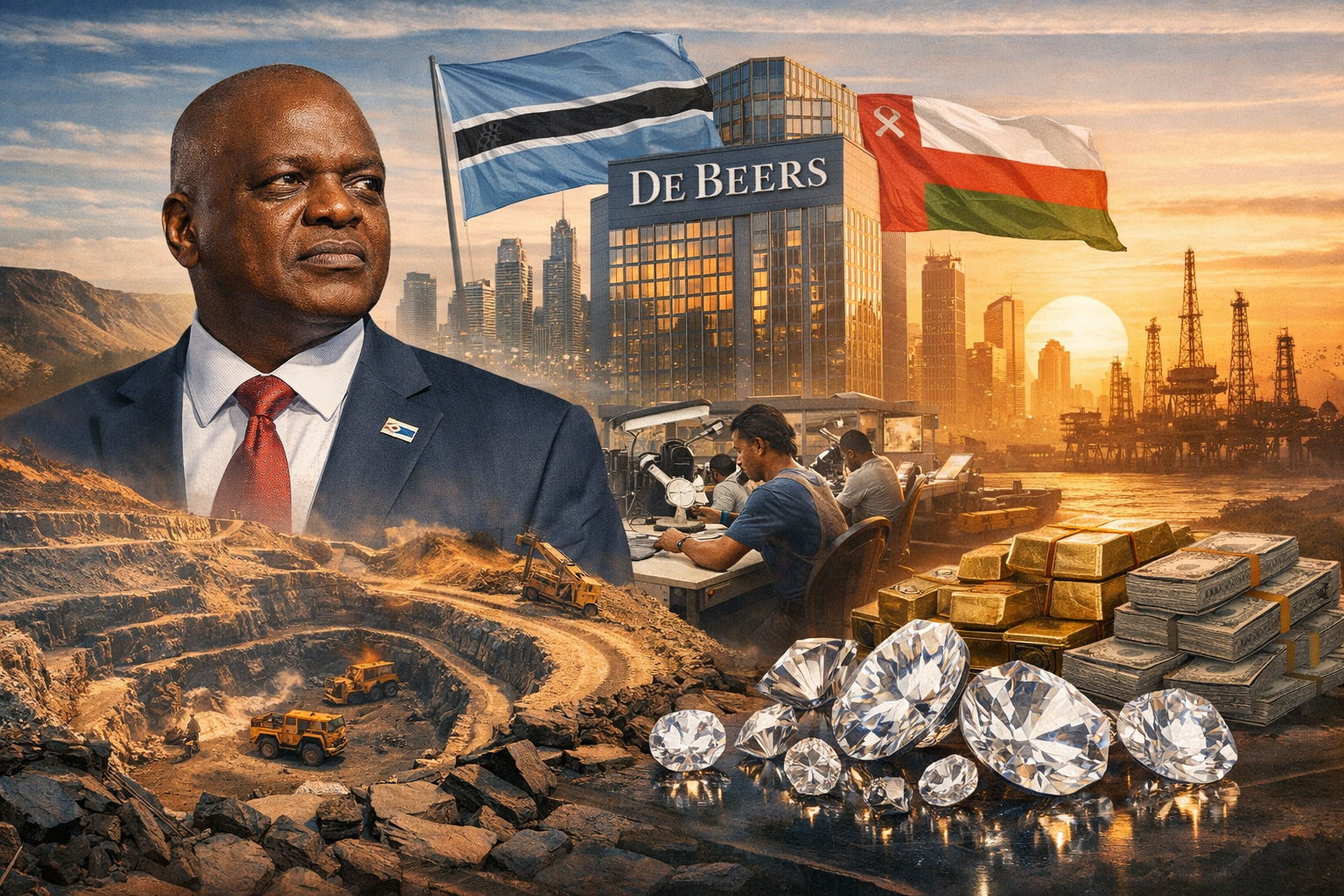

Botswana’s President Challenges De Beers for Greater Control of the Diamond Industry

Botswana’s escalating challenge to De Beers marks a defining moment in the global diamond sector, as resource-rich[…]

De Beers Group extends Desert diamonds into bridal with a new palette of lighter hues

Desert diamonds bridal campaign builds on the momentum of De Beers Group’s first new beacon in over[…]

World Diamond Day: The Most Valuable Diamonds Ever Sold at Auction

In recognition of World Diamond Day, we reflect on some of the most extraordinary diamonds ever offered[…]

Godfather of All Watches: $1.2m Tribute to Mafia Boss

Jacob & Co.'s Opera Godfather Baguette is more than a luxury watch set with almost 1,100 diamonds.

What Will Become of the Final Diavik Diamond?

Earlier this month, the Diavik Diamond Mine officially ceased operations, drawing to a close a remarkable 23-year[…]

Demand is “Resilient” as Phillips Hong Kong Raises $5.4m

Phillips raised $5.4 million from its Hong Kong Jewels Auction yesterday (30 March), reflecting what it described[…]

Botswana to Settle for Smaller De Beers’ Stake?

Botswana may now settle for a minority stake in De Beers rather than seeking majority control, according[…]

Botswana seeks to raise debt ceiling to weather diamond market downturn

Botswana’s finance minister sought parliamentary approval on Wednesday to raise the country’s statutory debt ceiling from 40%[…]

DCLA News | Botswana Doubles Down as Diamond Supply Tightens and Demand Strengthens

The diamond pendant worn by Bogolo Kenewendo at a recent Cape Town mining conference was more than[…]

De Beers Slashes Number of Sightholders

De Beers has reportedly slashed the number of sightholders who can buy their goods by as much[…]