Spending on luxury jewelry in May was up by 10.1 per cent, according to Citigroup.

The figure is strikingly at odds with the US Department of Commerce, which puts the year-to-year figure for May at just 2.9 per cent.

Citi, the third biggest bank in the US, bases its analysis of its 10m-plus US credit card holders. The Department of Commerce uses its own estimates, then revises its figures based on actual through-the-till transactions.

Citi also says luxury watch spending increased by 14.7 per cent. The Department of Commerce put the figure at 2.4 per cent.

Citi said the overall spend on luxury goods was weak but recovering in May, down 1.7 per cent year over year, compared with a 6.8 per cent decline in April and 8.5 per cent in March.

Luxury jewelry has consistently outperformed other luxury segments, such as handbags and apparel, since September 2024, according to the Citi data.

Jewelry was the only category to see both an increase in average spend per customer and a rise in the number of individual customers in May 2025.

Consumers are increasingly choosing jewelry over handbags and other luxury goods, which have seen less innovation and sharper price hikes.

ir David Beckham has one of the most recognizable wrists in the world. With tattoos reaching down to his fingers, it’s impossible to mistake his wrist for anyone else’s (even when he “accidentally” leaks an off-catalog Rolex). But not only was Beckham sporting something new and special at Wimbledon this weekend, he was doing so on a different wrist than usual—and he was more than happy to show it off.

David Beckham’s Unique Diamond-Set Tudor Chronograph at Wimbledon

First spotted in a reel posted by Adrian Barker of Bark and Jack, David Beckham has a new gift from Tudor to celebrate his 50th birthday—a unique Black Bay Chrono with a black lacquer dial, diamond indices, and case, bezel, and bracelet set with round diamonds. The legendary footballer has been a global brand ambassador for Tudor since 2017 and has show a lot of love for the brand, and it’s big sibling brand Rolex over the years, but its not often that we see unique watches out of “the Crown” or “the Shield” (though contrary to popular belief, they do exist) which makes this celebrity watch spotting historically noteworthy.

Barker was kind enough to send a few photos from his brief interaction with Beckham, and with them, we can pick out several interesting details about the one-of-a-kind piece. First, the black lacquer dial has been completely stripped of printing aside from the Tudor logo, “Tudor Genève,” and “Swiss Made” at the bottom. There is no minute track, and the subdials have also been stripped of numerals, resulting in a plain white reverse panda dial with small and long hash marks.

The bezel stands out with an unconventional design rarely seen on watches. The channel-setting of the round diamonds is done in pairs, with two rows of diamonds going all the way around. That, combined with the round diamond hour markers on sterilized black lacquer, gives a distinctly vintage feel that is more pronounced than you would get with a baguette-set diamond bezel. The lugs are set, as are the center links of the five-link bracelet.

There’s also rumor that the watch has two birthday candles in place of the number ”2” on the date wheel, for his birthday of May 2. The watch is cased in stainless steel and Beckham seems to be enjoying his new Tudor, even if he has to wear it on his left wrist for now. His right wrist (which he usually wears his watches on) is out of commission for a little bit as he recovers from surgery on a decades-old injury. Hoping he can recover quickly to wear his new watch in good health.

Lead photo credit Getty Images and Adrian Barker/Bark and Jack.

A collaboration by Pandora, the world’s biggest jewelry brand, and the e-commerce platform Amazon, has smashed a sophisticated counterfeiting network in China and led to the jailing of two crime bosses.

It also led to the seizure of thousands of fake Pandora jewelry items in a raid by Chinese law enforcement.

Pandora began investigating the source of counterfeit jewelry from China in 2020 after a series of customs seizures.

“It worked with counterfeit crimes unit at Amazon to identify two sellers operating a large-scale counterfeit network.

The probe led to the arrest and conviction of two people in March of this year. They were jailed for a combined total of five years and fined by a court in Shanghai for selling counterfeit items in several European countries.

Pandora, the Danish jeweler best known for its charm bracelets, said it was “committed to protecting our brand from the threat of counterfeit products”.

Peter Ring, senior vice president and general counsel at Pandora, said: “By combining our global brand protection expertise with Amazon’s investigative capabilities, we supported local law enforcement in dismantling a sophisticated criminal network.

“This case marks an important step forward in our ongoing efforts to safeguard the integrity of our brand and the quality our customers expect and trust us to deliver.”

Kebharu Smith, director of Amazon’s counterfeit crimes unit, said: “Counterfeiting is one of the oldest crimes in history, and we’re tackling it with our cutting-edge proactive tools and technology.

“Our collaboration with Pandora successfully dismantled a ring of bad actors, removing counterfeits from the broader supply chain.”

Amazon founder Jeff Bezos gave his new bride a pink 30-carat diamond engagement ring, valued at up to $5m.

He wed Lauren Sanchez in Venice, in a lavish three-day extravaganza (27 to 29 June) that reportedly cost $50m.

Bezos, worth an estimated $244bn, gave the ring to Sanchez, a journalist, philanthropist and helicopter pilot, when he proposed on his superyacht, Koru, two years ago.

The diamond, a cushion-cut pink diamond estimated to be about 30 carats, is set on a platinum band, secured by four prongs, with small stones set into the band and two pave halos. It was reportedly designed by US celebrity jeweler Lorraine Schwartz.

Experts put its value at $3m to $5m, depending on the exact specifications.

Sanchez reportedly wore an even larger white diamond at the wedding.

Bezos, aged 61, and Sanchez, 55, were both marrying for the second time.

Twin models and aristocrats Lady Amelia and Lady Eliza Spencer, nieces of the late Princess Diana, brought dazzling sophistication to Tiffany & Co.’s exclusive Blue Book High Jewellery Collection showcase, held atop The Harrods Helideck. The glamorous event marked one of London’s most prestigious evenings on the fine jewellery calendar, attended by fashion royalty and social elites alike.

The Spencer sisters, daughters of Earl Spencer, embodied modern British elegance as they arrived in bespoke Jenny Packham gowns paired with more than 150 carats of Tiffany & Co.’s finest high jewellery pieces—masterworks of exceptional diamond craftsmanship.

High Jewellery Spotlight: Eliza Spencer captivated in a silver mirror-embellished gown, perfectly complemented by the Ocean Flora necklace—an intricate platinum masterpiece featuring five unenhanced emeralds totalling over 10 carats, and a staggering 1,351 round brilliant diamonds totalling more than 44 carats. According to Tiffany & Co., this single piece took over 1,500 hours of artisan craftsmanship to complete, a testament to the meticulous design and precision that defines high jewellery.

Amelia Spencer wore a striking strapless black and gold sequinned gown and adorned herself with the same Tiffany necklace that supermodel Miranda Kerr wore to the 2025 Met Gala. The piece—a platinum and 18k gold choker set with Akoya pearls and diamonds—features more than 50 carats of gemstones, reflecting Tiffany’s modern reinterpretation of timeless elegance. Her ensemble was completed with diamond cluster earrings and a compact Aspinal of London Micro Hat Box bag.

Red Carpet Elegance Continues: Just one day earlier, the Spencer twins turned heads at the Serpentine Gallery Summer Party, wearing custom crimson gowns by Anamika Khanna Couture and showcasing statement diamond pieces by legendary Swiss house, Chatila. The event came just days ahead of the 31st anniversary of Princess Diana’s iconic appearance at the same venue—an enduring moment in royal fashion history.

A Legacy of Diamonds and Royal Style: The Spencer twins continue to honour their family’s legacy with graceful nods to their late aunt’s legendary style, but they are carving their own path in the fashion and jewellery world. Their presence at Tiffany’s high jewellery presentation not only highlighted the next generation of aristocratic style icons, but also reaffirmed the role of exceptional diamonds in telling modern luxury stories.

— At DCLA, we celebrate the enduring art of fine diamond craftsmanship. For more on gemological excellence and rare diamond showcases, stay connected to DCLA News.

US customs officers seized five shipments of counterfeit Cartier and Van Cleef and Arpels jewelry mostly from China, with a combined “if genuine” value of over $25m.

Almost 2,200 items – rings, earrings, bracelets, and necklaces – were intercepted by Customs and Border Protection (CBP) officers in Louisville, Kentucky, as they arrived in the country.

The first shipment arrived from China on 19 June, heading to a residence in Pennsylvania. Officers seized 318 bracelets with fake Cartier trademarks.

The second arrived the same day from Hong Kong, destined for a residence in Tampa with 490 necklaces, 205 pair of earrings, and 80 rings, all with fake Van Cleef and Arpels trademarks.

Three more shipments arrived from China the following day containing 800 “Cartier” bracelets. Two shipments were heading to a residence in Fayetteville, North Carolina, the other was heading to Michigan.

The 2,193 items were deemed to bear counterfeit marks,” the CBP said. “Had these goods been genuine, the five shipments would have had a combined manufacturer’s suggested retail price of over $25.32m.”

LaFonda D. Sutton-Burke, director of field operations, Chicago field office, said: “Intellectual property theft threatens America’s economic vitality and funds criminal activities and organized crime.

“When consumers purchase counterfeit goods, legitimate companies lose revenue, which can force those companies to cut jobs. Our officers are dedicated to protecting private industry and consumers by removing these kinds of shipments from our commerce.”

Red diamonds remain one of nature’s most elusive and captivating treasures. With only 24 specimens over one carat ever publicly recorded, their scarcity is legendary. Among them, the remarkable Winston Red has now taken centre stage at the Smithsonian National Museum of Natural History in Washington, DC.

This exceptional gem was donated in December 2023 by Ronald Winston, son of the renowned American jeweller Harry Winston. Weighing over one carat, the Winston Red is not only a visual marvel but also a scientific mystery—until now.

Recent research published in Gems & Gemology has provided unprecedented insight into what makes red diamonds so rare. Using advanced imaging and spectroscopic techniques, gemologists have identified that the Winston Red’s vivid crimson hue results from a combination of factors: a unique distribution of nitrogen impurities and a heavily deformed crystal lattice structure composed of tightly stacked red-to-pink layers.

These structural distortions—formed under extraordinary heat and pressure—are thought to alter the way light interacts with the diamond, giving rise to its intense red colour. Such conditions are extremely rare in the Earth’s mantle, further explaining the diamond’s scarcity.

Historical records trace the Winston Red as far back as 1938, when Jacques Cartier sold the stone to the Maharajah of Nawanagar. Combined with its cutting style and geological characteristics, the evidence suggests the gem likely originated from diamond-producing regions in Brazil or Venezuela.

For gemologists and collectors alike, the Winston Red represents both a scientific breakthrough and a pinnacle of natural beauty—an enduring reminder of the Earth’s ability to create something truly extraordinary.

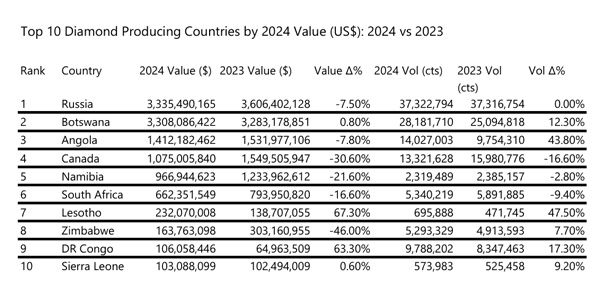

Russia remained the biggest rough diamond-producing country in the world in 2024, by both volume and value, despite the impact of G7 sanctions.

By volume it accounted for 32 per cent of global production in 2024 – or 37.3m carats – according to newly-released figures by the Kimberley Process Certification Scheme.

And by value it accounted for 29 per cent – or $3.335bn.

Botswana came second by volume – 24 per cent, 28.2m carats – and a very close second by value – 28.8 per cent, $3.308bn.

Overall global rough output fell 10 per cent to $11.48bn.

India was the biggest importer (40 per cent by carats, 39 per cent by dollars) followed by UAE (29 per cent by carats, 24 per cent by dollars).

Moscow investigators on Monday said they сharged an employee of the state-run diamond producer Alrosa, her son and two others in connection with a diamond theft scheme at the company.

Valentina Matyushenkova, an Alrosa employee, is accused of swapping high-value diamonds with cheaper industrial-grade stones between September 2024 and January 2025, according to Russia’s Investigative Committee.

Authorities say the stolen diamonds were smuggled to Armenia.

Matyushenkova was caught in the act while attempting to steal a batch of diamonds valued at more than 1.7 million rubles ($21,700), investigators said. Her son, Alexei Matyushenkov, is accused of acting as a middleman.

Two other suspects, Armen Petrosyan and Arman Sahakyan, allegedly transported the stolen stones across the border to Armenia.

A video published by the Kommersant business newspaper showed Matyushenkova confessing to her role in the scheme during questioning. One of the other suspects claimed he was working as a deliveryman at the time of his arrest.

Searches of the suspects’ homes uncovered some 200,000 carats of low-grade industrial diamonds, which investigators say were used to replace the high-quality raw stones.

All four suspects have been placed in pre-trial detention. If convicted, they face up to 10 years in prison on theft charges and up to seven years for the illicit trafficking of precious stones and metals.

A 275-year-old carved emerald necklace from the Mughal Empire sold for $6.2m, more than double its high estimate, at Christie’s New York.

It is made of five Colombian emeralds, with a combined weight of 1,178.50 carats (8.3oz/235g) on gold and magenta cords.

Three are carved hexagonal – the largest is 470 carat and inscribed “Ahmad Shah Durr-i Durran” (Pearl of Pearls) – and two are carved pear-shaped.

The necklace once belonged to Nader Shah, one of the most powerful rulers in Iranian history, and one-time owner of the Koh-i-Noor diamond.

He seized the necklace after capturing Delhi in 1739 and taking control of the royal treasury of the Mughal Empire, which ruled much of the Indian subcontinent from 1526 to 1857.

The necklace carried a pre-sale estimate of $2m to $3m.