How to Clean a Diamond Ring at Home – Expert Advice from DCLA Diamond laboratory

Has your engagement ring lost its brilliance? Don’t worry—your diamond hasn’t lost its sparkle. It simply needs[…]

De Beers Reports $511 Million Loss as Global Diamond Crisis Deepens

Despite generating approximately $3.5 billion in revenue, profitability deteriorated sharply, highlighting a widening disconnect between stable turnover[…]

Halle Berry Follows Celebrity Trend for Vintage Diamonds

Halle Berry shifted the focus back to vintage diamonds with her latest engagement ring.

What Is a Diamond? Natural vs Laboratory-Grown – Structure, Science and Pricing

A diamond is a solid form of the element carbon in which the atoms are arranged in[…]

Diamond Slowdown: Expansion at Gahcho Kue is “Paused”

Mountain Province Diamonds (MPD) say it has "paused" plans for a key expansion that would have prolonged[…]

Love that lasts: natural diamonds continue to win hearts, with 2.1% growth in speciality jeweller sales

Diamonds embody enduring love, making them the natural choice for marking a relationship.

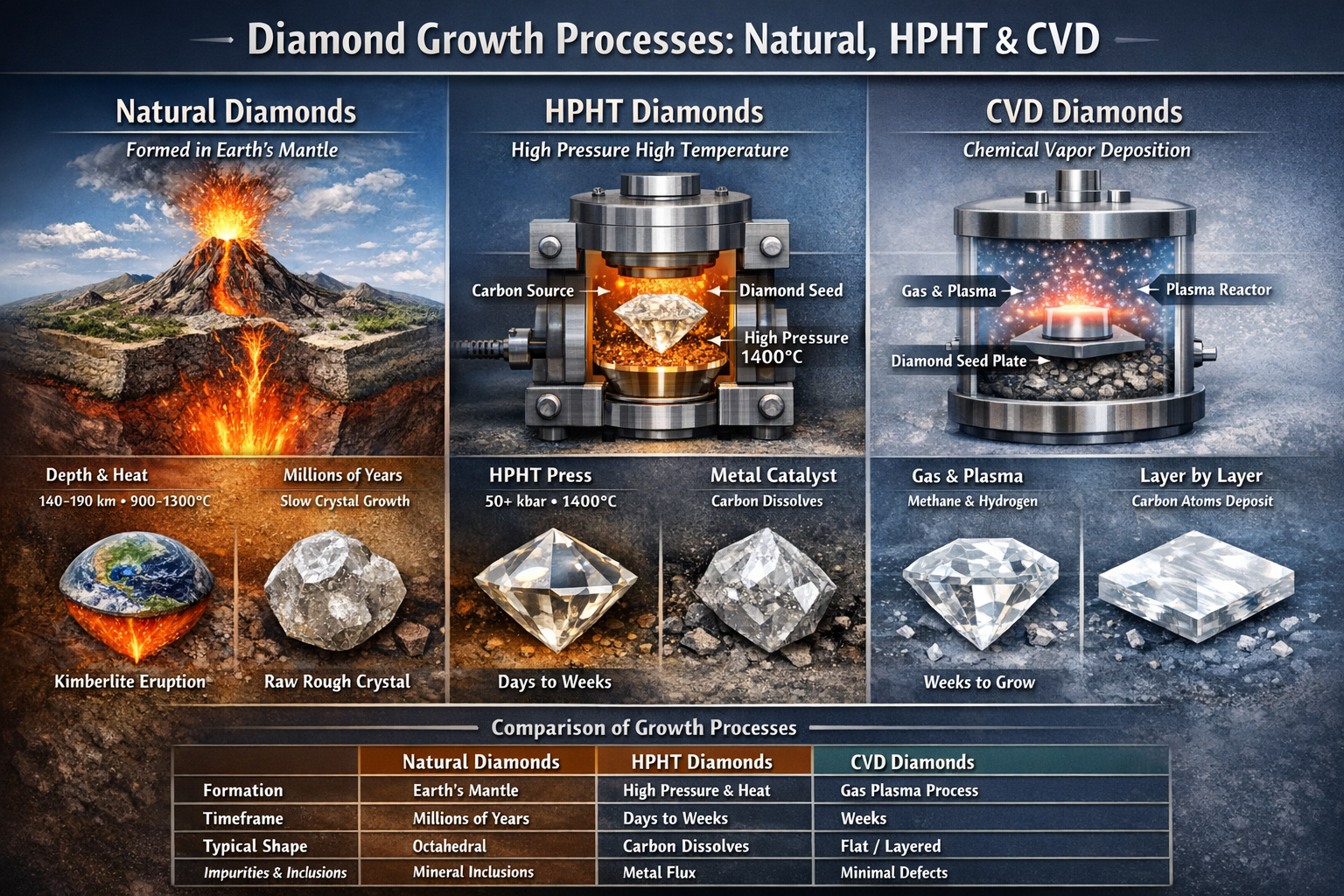

Understanding Diamond Rough Growth for Natural, HPHT and CVD Diamonds

Naturalmined, HPHT, and CVD Rough Diamonds

IDEX Price Report: Further Drops for Rounds and Fancies

Price drops dominated yet again both for rounds and fancies during January, as US tariffs on India[…]

Gems set to retain sheen, view cloudy for diamonds after US tariff cut

Washington's reciprocal tariff reduction is expected to help India's gems and jewellery exporters regain lost ground in[…]